by John Harbison, TCA Chairman Emeritus

(originally published by the Angel Capital Association in their Data Insights Series)

We all know that investing in early-stage companies is a very risky proposition, and the majority of investments will either fail completely or fail to return the capital invested.

The reasons for failure are diverse, but almost never due to fraud. Unfortunately, the intense media coverage of a few spectacular failures such as Theranos and FTX (and the fraud associated with them) have sadly led many policy makers in Washington DC to conclude that fraud is rampant in this asset class and therefore further regulation is necessary to help “protect” investors. This perception is a remarkable misunderstanding, and this article will present data and analysis to set the record straight. It is also regrettable since some of these notable failures (such as Theranos) never received funding from any organized Angel Group, all of which follow a rigorous due diligence process, so in that sense there is not a prevalent problem with fraud in investments by Angel Groups after appropriate due diligence.

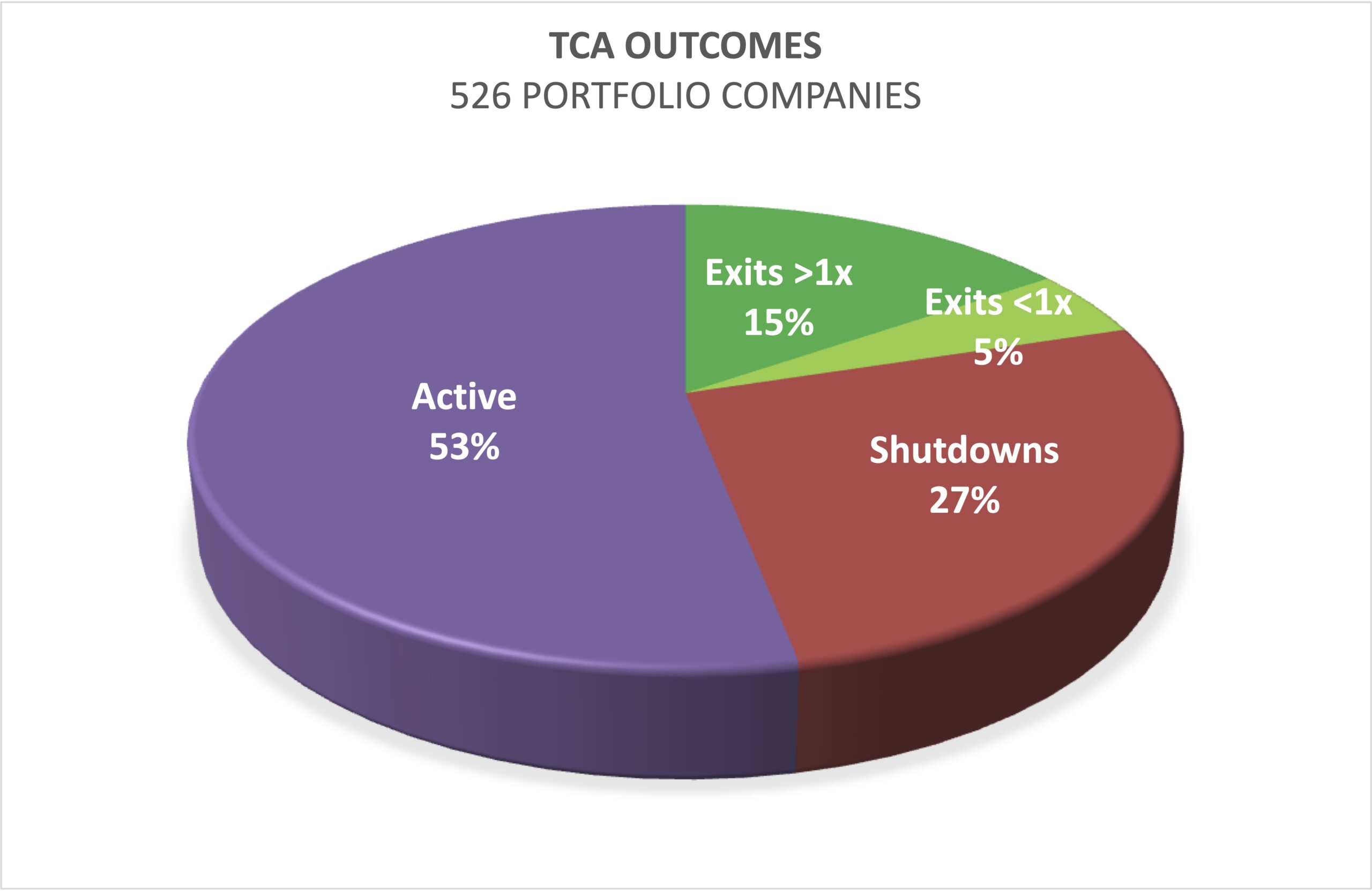

Many studies have shown the failure rate in this asset class is over 50%. For Tech Coast Angels, 32% of the companies and 68% of the outcomes failed to return the capital invested:

Source: All Tech Coast Angel portfolio companies through 2022

For individual TCA members, the failure rate varies widely, partly due to some members having a higher proportion of recent investments — hence fewer outcomes:

Source: June 2023 Survey of Tech Coast Angel members

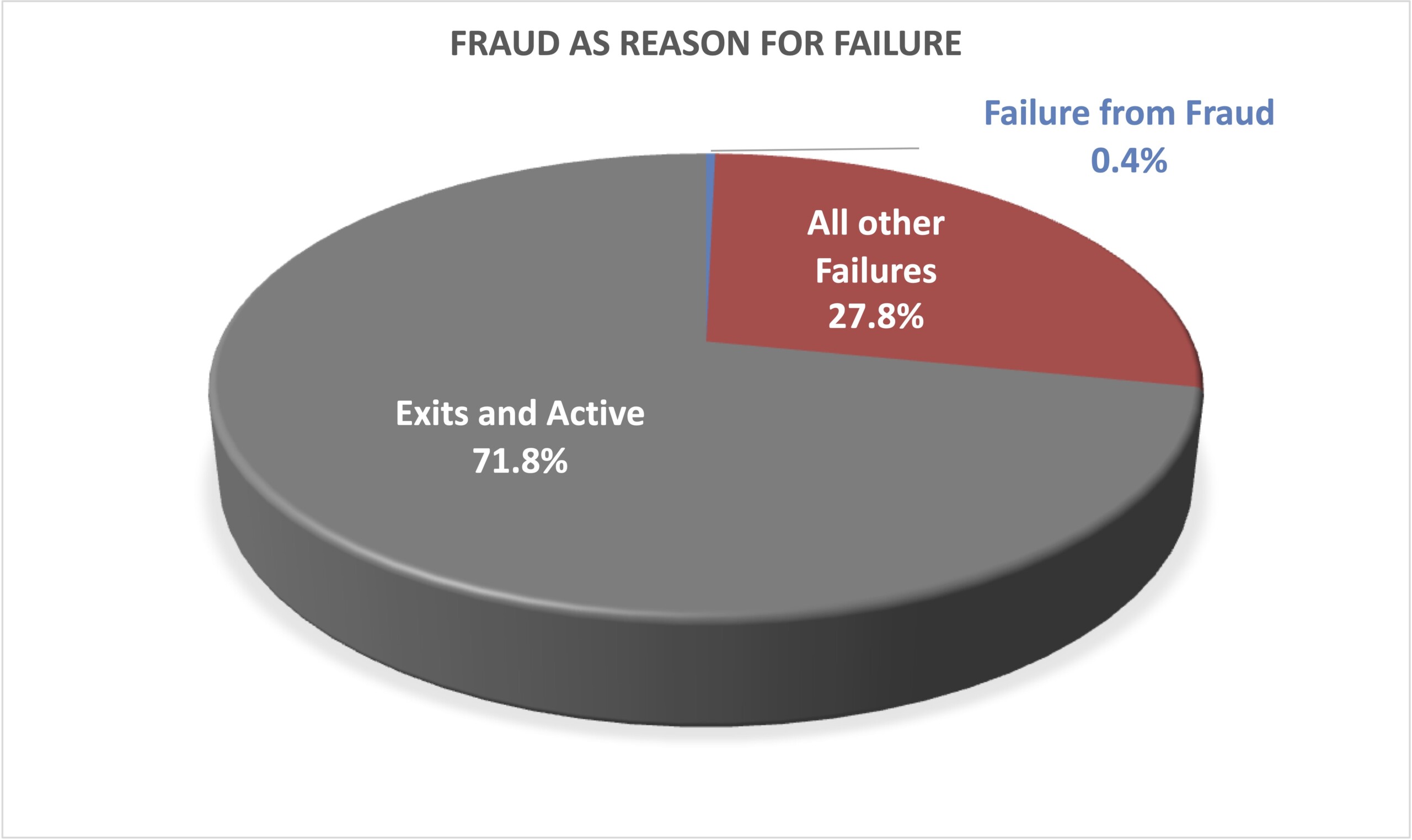

But of those failures, less than half a percent were due to fraud. This is based on a recent survey of TCA members in which 107 members indicated 2733 investments and only 10 were related to fraud (and all 10 were investments in the same “alleged” fraudulent company):

Source: June 2023 Survey of Tech Coast Angel members

Fraud obviously comes in many flavors such as Ponzi schemes, misrepresentation of financials, embezzlement of funds aka payroll fraud, overvaluation of assets, misuse of investment funds, false customer or partnership agreements, exaggerated market traction, fabricated intellectual property claims, unreported conflicts of interest, falsifying financial statements to misrepresent the company’s financial health and performance, vendor fraud, inventory theft or misappropriation, expense reimbursement fraud, fake invoices and billing fraud. However, it typically does not include overly optimistic communications from the CEO to investors; many companies as they go into their final spiral before acknowledging failure have the problem of claiming things look better than they are, but few people consider those rose-colored glasses “fraud.”

Not withstanding the high overall failure rate, a sufficiently diversified portfolio of early-stage investments can yield attractive returns. Since TCA’s founding in 1997, there have been 247 outcomes including 106 exits and 141 shutdowns. If you’d invested an equal amount in all 247 of those companies, you would have received a cash return amounting to 6.4 times your investment and an IRR of 25%. But as is the case in early-stage investing, a small percentage of investments make for most of the return. Six of the exits were from 58x to 368x and missing all of these six drops the TCA portfolio return to 1.8x and 9.3% IRR. This is why diversification is so important. For more on this, see a previous insight on “Angel Returns Beat All Asset Classes But Pose Greater Risk.”

KEY TAKEAWAY

Failures are quite common in early-stage investing, but the reason for failure almost never is because of fraud. While fraud equates to failure, failure does not equate to fraud: It is critical to understand that failure comes in multiple non-fraudulent forms.